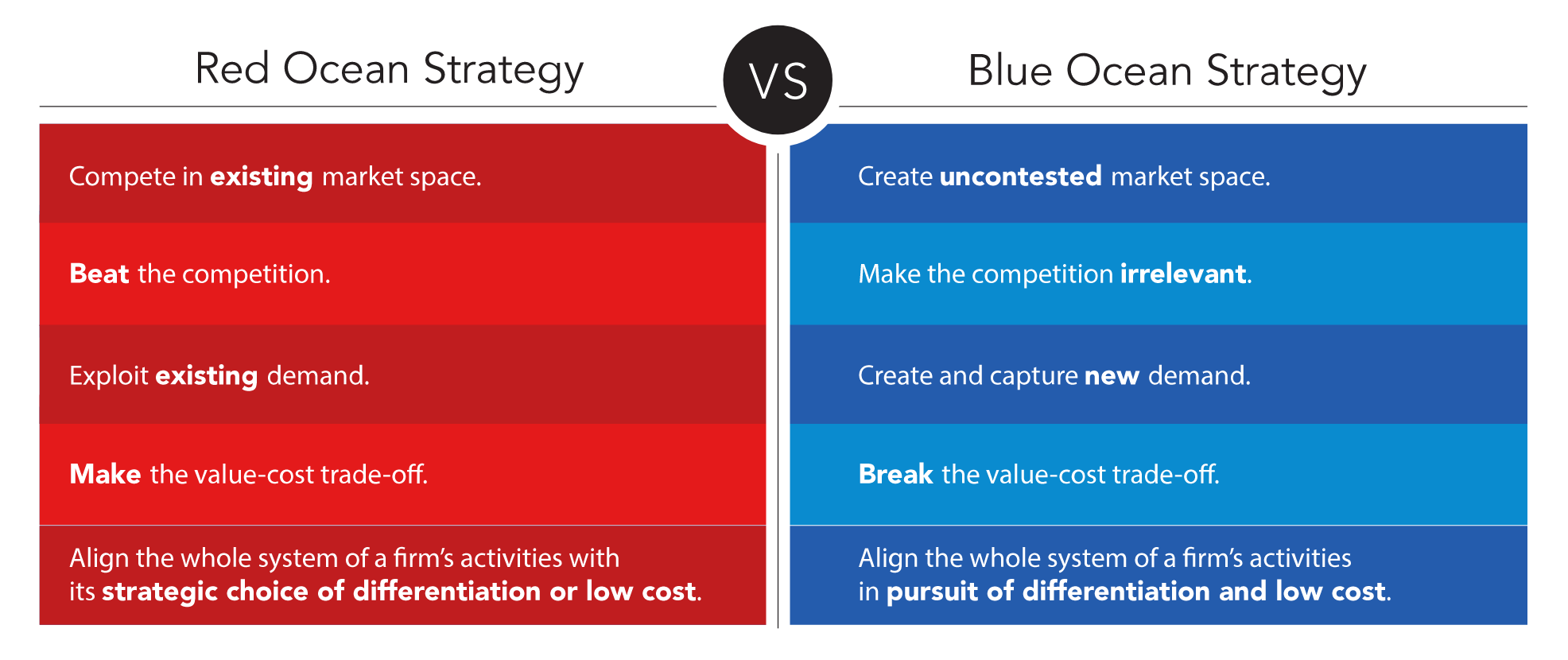

Over a decade ago, INSEAD business strategy professors W. Chan Kim and Renée Mauborgne popularized the terms “blue ocean” — untapped markets where “demand is created rather than fought over”, enabling profitable growth — and “red ocean” — zero-sum markets, where every fluid ounce of demand is bitterly fought over, like sharks fighting over a whale carcass.

The early ridesharing market was a deeply red ocean, plagued by price wars, rife with cutthroat tactics, and littered with failed startups.

However, many entrepreneurs and investors initially saw a blue ocean in the early ridesharing market. Ridesharing was a new, unexplored medium that promised to revolutionize and expand the ground transportation market wherever mobile devices were ubiquitous by “unlocking” pent-up demand for one-tap transportation.

As a young investor, I balked at this characterization. While I agreed on the long-run impact of these next-generation transportation networks, I thought this view was dead wrong in the short-term.

Here’s why.

Receive my next thought in your inbox

Demand-driven market growth

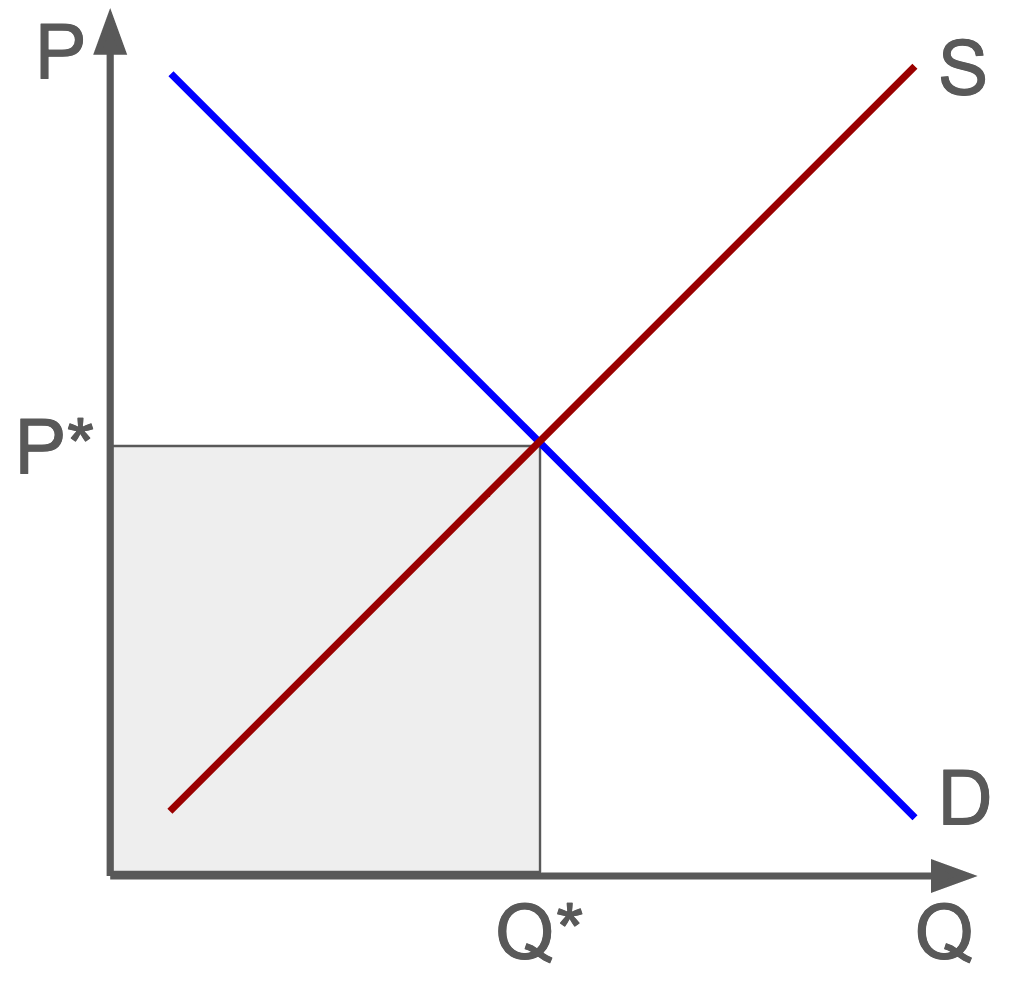

In the simple Economics 101 model of supply and demand, market growth comes in two flavors: demand-driven and supply-driven, characterized by increased willingness to buy or sell respectively at a given price.

Many people miss the subtlety that the cause (supply or demand) behind the effect (growth) impacts how attractive a market is to new and existing entrants.

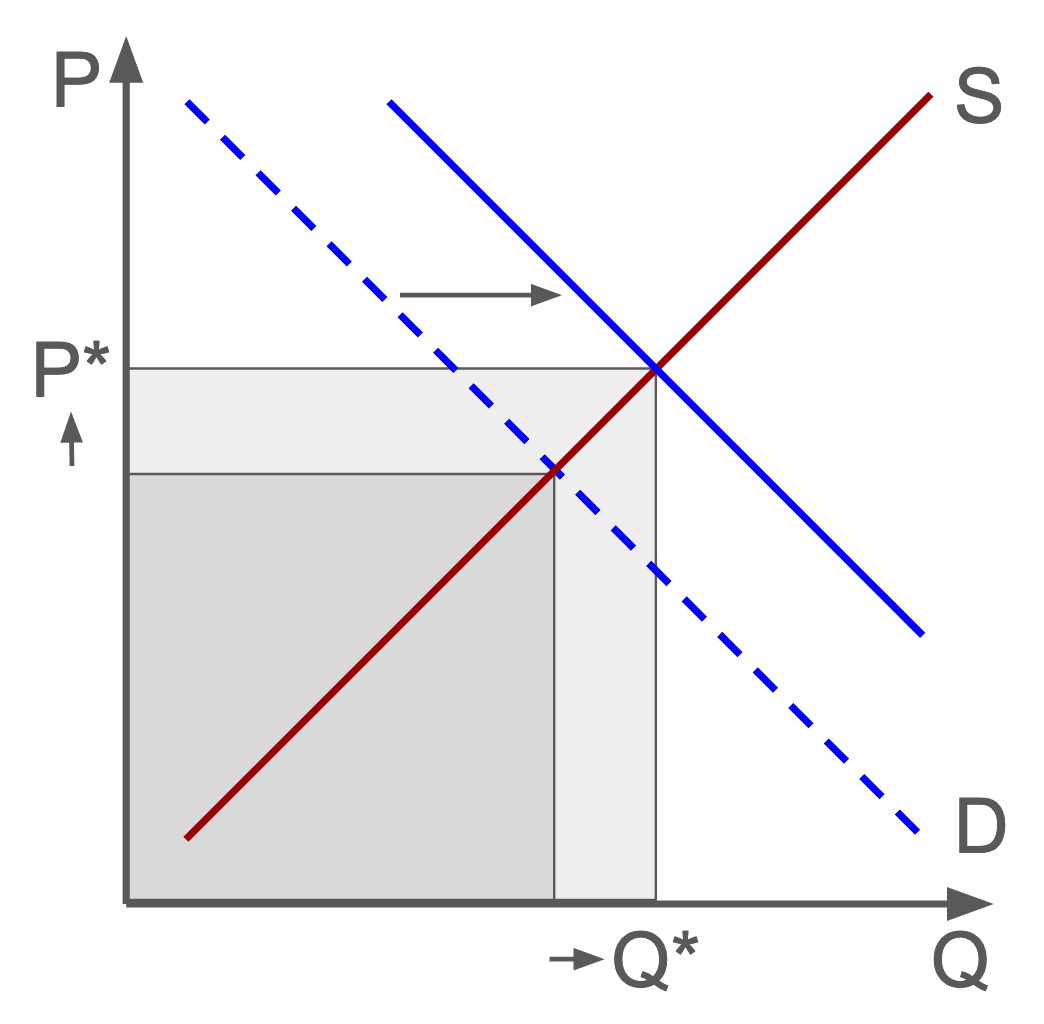

More demand translates into both higher prices and volume transacted. Hence, markets growing due to a buildup of demand are highly attractive to new entrants, as businesses can grow without necessarily taking share from others and avoid contentious, competitive battles over market share.

Even with the arrival of new competitors, as long as the increased in demand outstrips the increase in supply, prices, and therefore profits, will be stable or increasing, and we’ll see higher volume of transactions regardless.

This is both exciting to new market entrants and encouraging for existing suppliers.

Demand-driven growth is intuitive. It's what most people associate with a growing market. It’s easy to assume that market growth always comes from consumers demanding more.

Supply-driven market growth

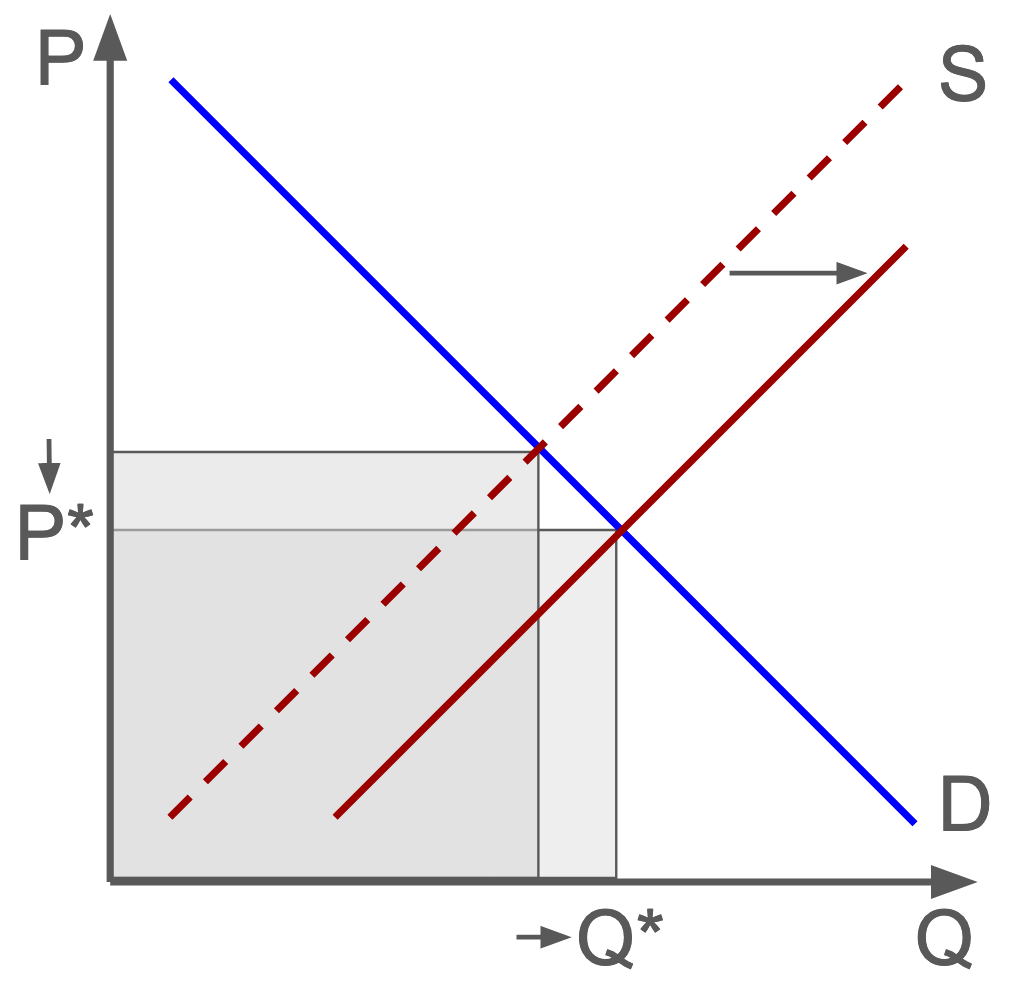

However, the sudden growth of ridesharing is better explained by activity on the supply-side — the founding of Uber, Lyft, and an eclectic cast of competing startups, all focused on the same market, the same core idea.

Ridesharing was not a demand-side phenomenon. The market was itself created by the supply-side, which then generated supply-driven growth.

Supply-driven market growth causes prices to decline rather than increase. These price cuts eat away the profitability of suppliers and bar others from entering the market who cannot viably operate at these lower prices — like a sea wall breaking waves before they hit the shoreline.

Further, gaining share requires either fierce competition along the product or marketing dimension or aggressive price cuts. Market share must either be taken from other suppliers, who originated the market growth in the first place, or created by offering the same or better product at lower prices.

The ridesharing market spawned out of the emergence of these new services — new sources of supply.

What funded this Cambrian explosion of ridesharing? Venture capital.

Capital is a key competitive advantage due to its ability to fund continuous price subsidies. These artificially deflated prices both undercut capital-constrained competitors and drive consumer usage.

Prices down, volume up.

The flood of new customers impresses other investors and attracts more funding, enabling the early winners to cut prices further. Additionally, the increased ridership attracts and retains drivers, whose earning power is enhanced via two-sided network effects about which much has previously been written.

This completes the virtuous cycle:

Initial innovation → venture capital → lower prices → more usage → venture capital

Swimming with sharks

Lyft and Uber correctly saw the nascent ridesharing market as a red ocean. Despite dreams of a future where spend would shift from personal car purchases to ridesharing, they could not afford to wait for demand to arrive. In the near-term, supply would outpace demand, making the market much more competitive.

Appropriately, Uber and Lyft armed themselves for the fight, raising “war chests” of capital to fund a ridesharing “arms race”.

Uber and Lyft expanded aggressively into new cities at a breakneck pace. They cut prices, then cut them again, and just kept on cutting. Already market leaders, they spent generously on cash bonuses and other driver incentives.

In contrast, their early competitors bought into the eventually-true-but-not-yet promise of a world transformed by app-based transportation, hoping to surf the seemingly blue ridesharing wave.

Nothing wrong with being a small fish in a big, blue pond, right?

These hapless ride-surfers didn’t realize supply-side sharks like Uber and Lyft were the entire reason for the wave in the first place.

How did this tidal wave impact other ridesharing startups?

- Unable to match the subsidized prices, other players failed to attract users

- Fewer customers meant lower driver earnings, leading to an exodus of drivers

- Sparse supply on the driver-side lengthened wait times, degrading the rider experience, pushing more of them away

- Declining usage scared off new investors

- Incapable of raising fresh funds, the other fledging ridesharing startups, metaphorically, drowned.

The “blue ocean” turned red; the virtuous cycle turned vicious.

Acting with haste and fervor, Uber and Lyft established an insurmountable lead, effectively eliminating their U.S. competition before changing norms and consumer behavior on the demand-side had a chance to catch up.

In other words, they saw red where others saw blue.

Lessons learned

A few key takeaways:

1. Supply is red, demand is blue

- A merely growing market is not necessarily an attractive one

- The drivers of growth matter more than the level of growth

2. The deep sea requires deep pockets

- Capital can often be converted directly into market share

- Red ocean markets demand significant capital, as growth is unprofitable in the short-run

3. Cheap capital and disruptive innovation create supply-side tsunamis

- When capital is inexpensive, supply reacts to innovation much faster than demand

That the ridesharing market could consolidate so early in its existence is remarkable but also perhaps predictable if one understands it’s supply-side origins.

And despite an evolution of norms around getting into a stranger’s car, Uber and Lyft are betting big on another supply-side innovation: autonomous vehicles.

Why? Again: to push out the supply curve, drive down prices, expand usage, attract capital, and reinvest in more robotaxis.

In other words, it’s the same supply-driven growth story all over again.

That the two ridesharing leaders continue to operate unprofitably at scale only further drives the point home. This is not a demand-side story and never has been.

This is a cautionary tale for entrepreneurs and investors clamoring to capitalize on the latest “wave”.

Sometimes, the right kind of rose-tinted glasses isn’t such a bad thing.