COVID hurt most software companies.

While many claim COVID accelerated technology adoption and digital transformation, this didn't show up in the revenue of most software vendors.

In fact, the typical public software company remains 10-12% below its pre-COVID revenue trend, and the gap is only widening.

COVID put most software companies on a permanently lower growth trajectory.

Receive my new long-form essays

Thoughtful analysis of the business and economics of tech

A few case studies

The COVID shock generated divergent outcomes across software companies.

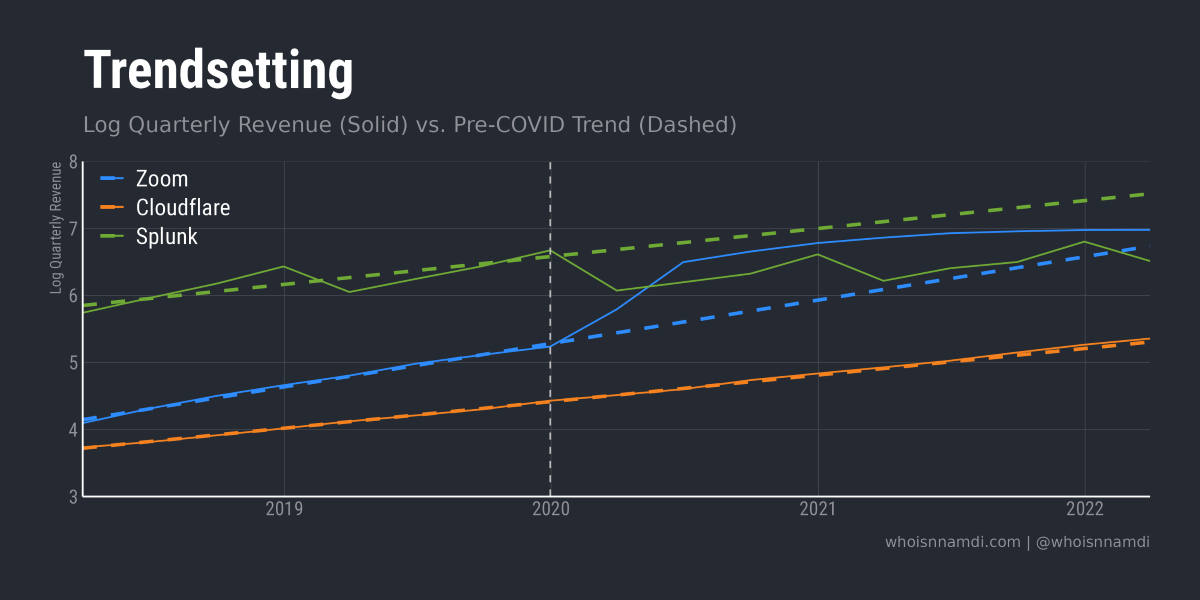

Let's focus on three examples to see what I mean: Zoom, Cloudflare, and Splunk.

The solid lines below represent the (log-transformed) quarterly revenue of each company. The dashed line represents a constant-growth linear trend based on their two-year pre-COVID revenue trajectory. Since the scale is in logs, straight lines imply constant quarter-over-quarter growth:

We see some interesting behavior as we cross the dashed line, which represents Q4 2019, the last quarter before COVID struck:

- Zoom immediately takes off, "zooming" above its pre-COVID trend as millions move to online communication. The trend eventually catches up

- Cloudflare is totally in the clouds, floating along like nothing happened, perfectly matching its pre-COVID trend of constant, exponential growth

- Splunk exhibits strong seasonality, so the initial decline is no surprise. However, it never recovers to trend, even two years later. Splunk got dunked

These symptoms run the gamut from manic to lethargic. Clearly, COVID was not a tide that raised all boats.

Mean reversion, or mean revision?

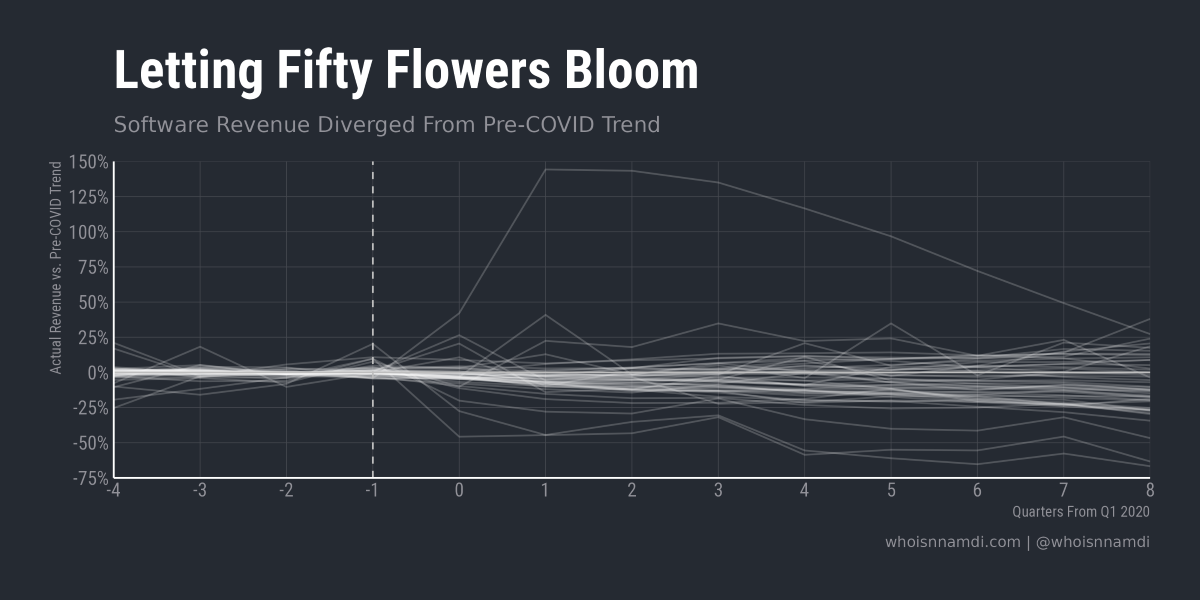

We can repeat the above analysis for all public software companies with enough data to establish a two-year pre-COVID trend. Given the different revenue scales, for visualization purposes let's normalize by dividing each company's actual performance by its extrapolated trend. This gives us the relative revenue performance of each vs. trend:

Each line represents performance vs. trend for one of fifty different public software companies.

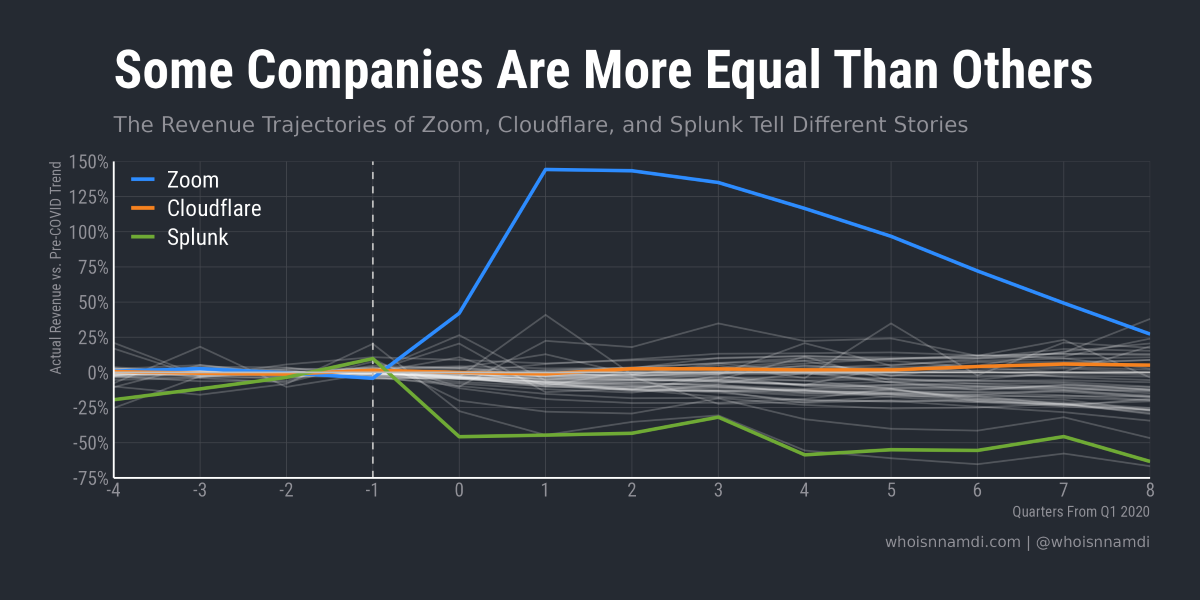

With this we can begin to see the rich variety of post-COVID outcomes. Let's highlight our three case studies once more:

- Notice how dramatic and unrepresentative Zoom is among all software companies. Zoom peaks at ~150% above trend before gliding back down to Earth

- On the other hand, Splunk comes out as one of the worst performers, among others like Alteryx and Benefitfocus

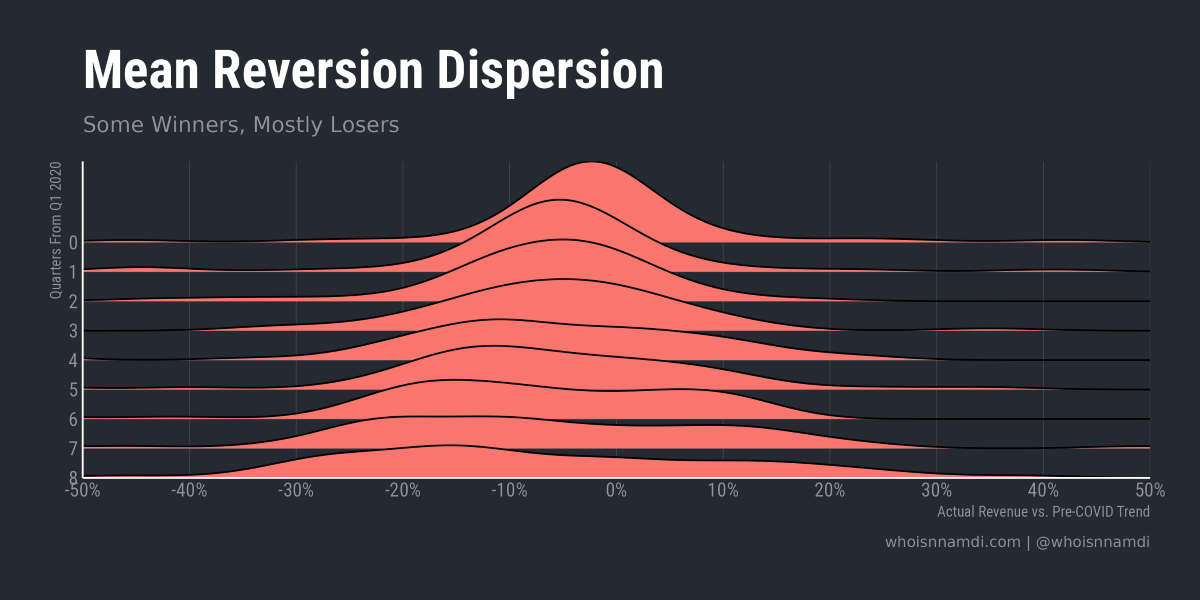

There's a lot going on here, making it difficult to get a sense of the underlying distribution. Let's flip the axes and look at it a different way:

The above chart plots histograms of performance relative to trend across public software companies from Q1 2020 onward:

- Upon impact, performance is normally distributed, centered somewhat below zero

- Over the subsequent quarters, the distribution shifts left and widens, implying worse outcomes and greater dispersion between companies

- By eight quarters out, performance is unambiguously below trend, while variance continues to grow

Notice the skew: a handful of winners among a majority of losers.

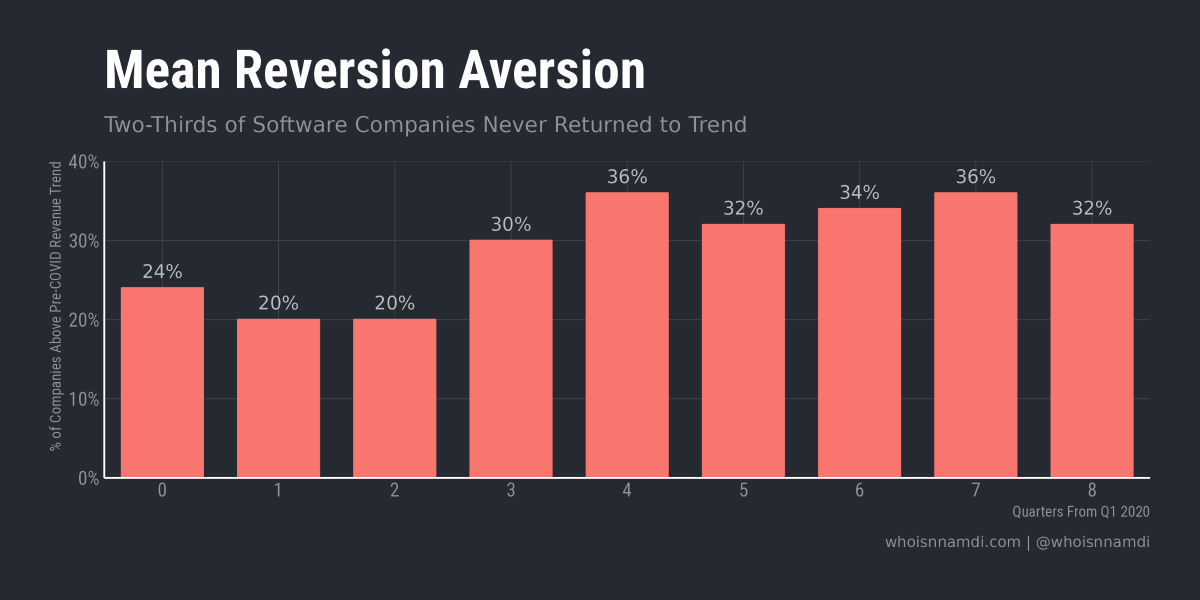

Another way to look at the data is to calculate the proportion of software companies that climbed above their pre-COVID trend over time:

- Initially, only a quarter of software vendors were above trend

- One year out, one-third of companies have returned to trend

- The proportion stabilizes thereafter. Mean reversion is over

This is interesting. As dispersion grew in the first year of the pandemic, some companies returned to their pre-COVID trend. After these initial quick recoveries, however, mean reversion completely shuts down. The last lifeboats cast off, and if you aren't onboard, you're ngmi.

A key point I want to drive home: mean reversion is a strong force, but COVID was stronger, especially on the downside. Once knocked down, the typical software business never got back up.

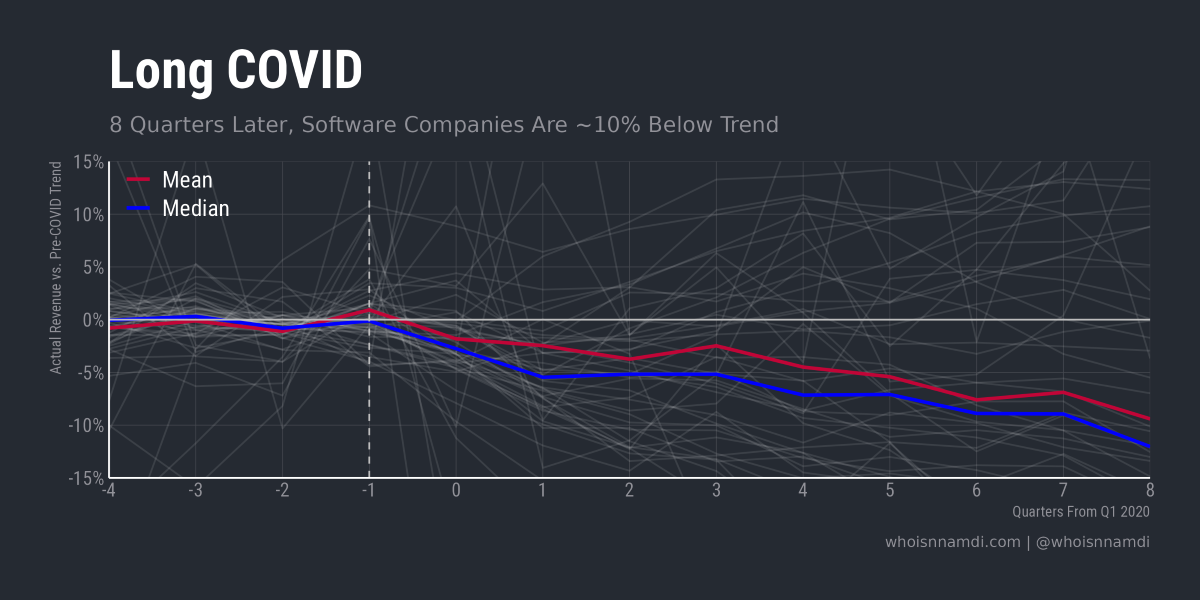

Weakness, in numbers

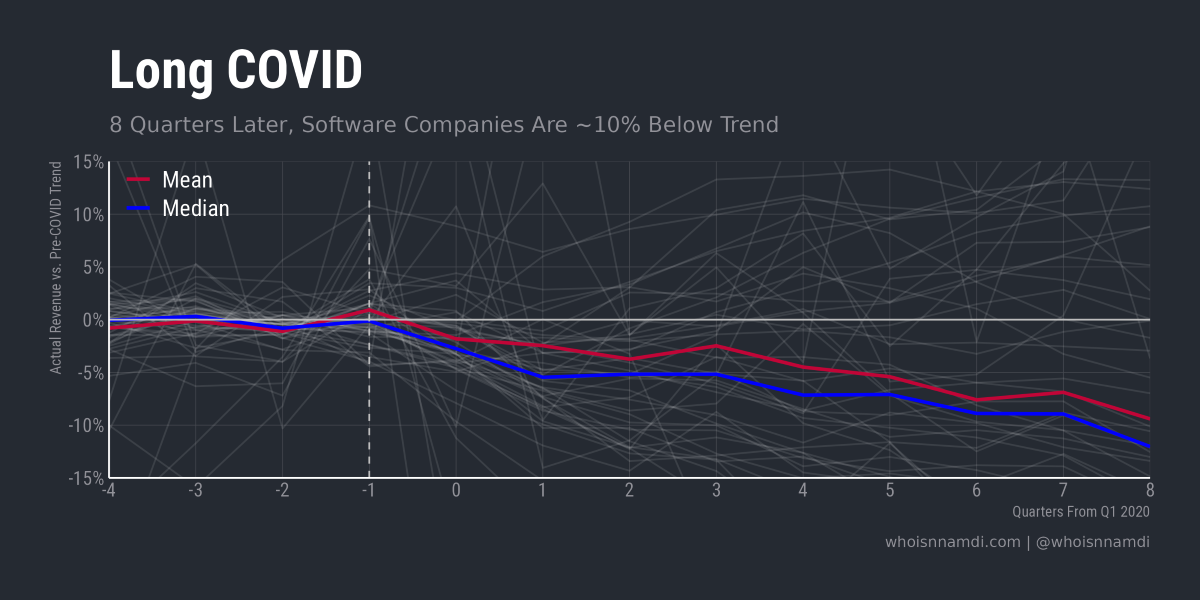

Finally, let's summarize those performance distributions by their means and medians:

This is what I've been building up to – COVID materially impaired the typical software company, knocking it off trend:

- On average, software companies were down ~5% relative to trend 4 quarters out and down ~10% 8 quarters after impact

- The median dampens the impact of outliers like Zoom. Notice, median performance is even worse, ~7.5% at 4 quarters and ~12.5% at 8 quarters

- Meanwhile, underperformance relative to trend is still increasing. The gap between actual revenue and trend is growing ~4% per year

Thus, COVID's impact was not transitory: COVID permanently reduced the annual growth rate of public software companies by 4 percentage points.

Mean revision is at least as important as mean reversion. Not only are software companies below their pre-COVID trend, the trend itself has changed for the worse.

Conclusion: Conflation

I think there's been a massive conflation between:

- the equity returns of software companies during the first year and half of COVID (exceptional, but temporary),

- the financial performance of a select few COVID beneficiaries like Zoom (again, exceptional, but transitory), and

- the business performance of the broader software market (poor, and durably so)

The temporarily exuberant stock prices of most software companies distracted from the toll COVID took on business performance. While investors got high on the Fed's supply, businesses themselves were silently suffocating.

This corroborates the findings of my last essay, where I explored how the mysterious "GDP factor" explains some the the "dark matter" in software valuations:

Despite some claims to the contrary, investors believe software companies are quite sensitive to the broader macroeconomic environment. In fact, it's the variable that correlates most highly with valuations after accounting for the individual financial performance of each company – The Dark Matter of Software Valuations

Here again, I find that software companies are sensitive to economic conditions, even in a best case scenario that supposedly favored them. "Digital transformation" can't come quickly enough it seems.

So let's set the record straight: COVID left a nasty scar on us all, software companies included.

Receive my new long-form essays

Thoughtful analysis of the business and economics of tech